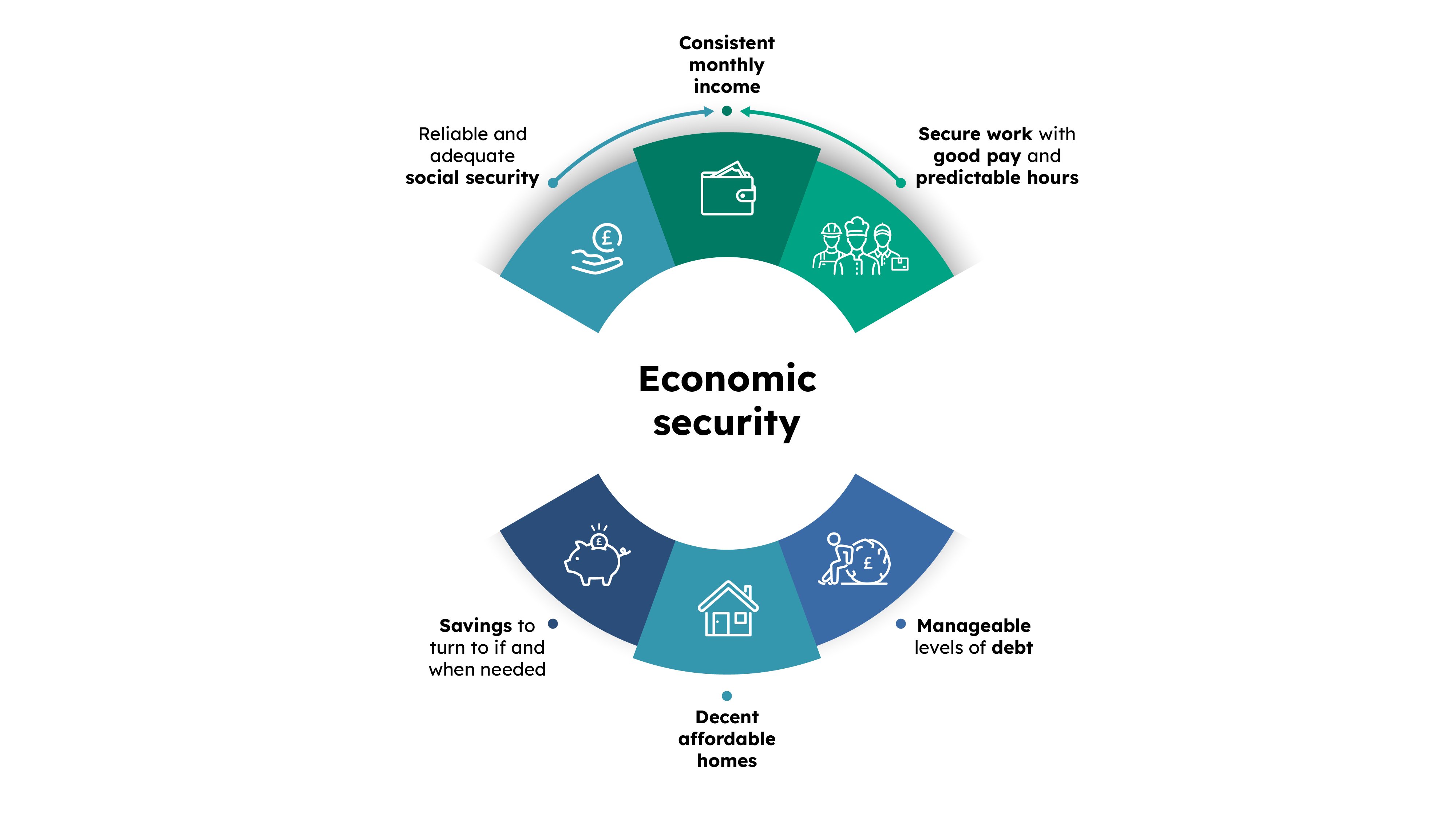

The building blocks of economic security in Scotland

This briefing explores what is driving widespread feelings of economic insecurity in Scotland today.

- Written by:

- Date published:

- Reading time:

- 18 minutes

- 1. Introduction

- 2. Income as a building block to economic security

- 3. Good work as a foundation for economic security

- 4. Knowing you will have a roof over your head

- 5. Savings as a safety net

- 6. Needs and expectations change over the life course

- 7. Conclusion

- Method

- References

- How to cite this briefing

- 1. Introduction

- 2. Income as a building block to economic security

- 3. Good work as a foundation for economic security

- 4. Knowing you will have a roof over your head

- 5. Savings as a safety net

- 6. Needs and expectations change over the life course

- 7. Conclusion

- Method

- References

- How to cite this briefing

1. Introduction

Everyone in Scotland should be able to live their life without worrying about whether they will be able to pay their next bill or put food on the table for their family. The feeling of security this gives is an essential foundation for a good quality of life. But for far too many people, that is not the case.

Our analysis has shown that nearly half (47%) of adults in Scotland feel economically insecure and this is driving political disaffection across the country (McKenzie and Cebula, 2026). There is often a misconception that economic security is determined only by income. While income is obviously crucial to whether people can afford daily living costs, it is equally important to consider the extent to which people have access to a wider financial safety net.

Here we break down these different building blocks of economic security to paint a picture of why it is missing for so many people in Scotland today. We show how the combination of income, housing, work, savings and debt, determine how secure people feel in their finances. Much like poverty, economic insecurity is not a fixed state in people’s lives. Life circumstances change in expected ways as people age, and in unexpected ways, for example, due to job loss or ill-health. We look at how economic insecurity affects people in different ways over the course of a lifetime, emphasising the importance of having a financial safety net to fall back on.

We should find it worrying that so many people in Scotland are concerned about their standard of living, both now and in the future. If left unaddressed, we risk seeing this far-reaching feeling of instability become further entrenched in the outlook for Scotland. This is important, not only for families, but for the future of politics too. These findings should urge politicians, and ultimately the next Scottish Government, to tackle poverty and economic insecurity and demonstrate that politics can be the catalyst for better living standards.

2. Income as a building block to economic security

The amount of money regularly coming in helps us to meet our day-to-day expenses but is also an important part of building up other components of economic security, such as buying a home or putting money aside in savings. It’s important to remember in this section that while income helps families build other components of economic security, not all people will have the same combinations of components. In addition to this, we know that feelings of economic security are also influenced by individual experience and broader economic challenges experienced in our society.

Half of people in the bottom equivalised (before housing costs — BHC) income quintile are feeling economically insecure, meaning that they were worried about their family's economic security. We also measured economic security using a number of questions covering respondents’ worries about their income, savings, debts, housing and work to identify people who are very economically insecure. We see greater variation in the proportions who are very economically insecure across income quintiles, with around 1 in 3 (32%) people in income quintile 1 compared to 16% in income quintile 5.

Looking in more depth at some of the key questions that made up our definition of very economically insecure, we see that lower-income households are feeling more uncertain about their current, and future, financial situation. People in the bottom income quintile are more likely to be worried about their household income, and less likely to feel confident they can cover the essentials than higher-income quintiles. They are almost half as likely to say they are satisfied with their amount of savings compared to people in the highest-income quintile (27% vs 52%). Looking forward, just 1 in 3 (34%) are confident they can have a decent standard of living in old age compared to 59% of people in the top income quintile. We also see that workers in the bottom income quintile (34%) are more likely to be worried about keeping their job than other income groups.

We asked respondents to select the top areas that would make the biggest difference to their own economic security. Across income quintiles, the top 3 were consistently lower cost of essentials, higher pay and improved pension savings. However, there were some variations in preferences further down the list across income quintiles:

- for lower-income households, solutions around the social security system and support with debt were selected more compared to higher-income quintiles

- for higher-income quintiles we see good work (both security, and terms and conditions) and childcare higher up the list of solutions

- there is a greater spread across the solutions for people in income quintile 1 than other quintiles, reinforcing that the drivers of economic insecurity go beyond household income.

This shows political parties that addressing living standards is a top priority among voters across the income distribution, with broad support for policies that improve living standards across the life course.

Having a higher income generally creates a buffer for people to cover everyday costs, build up more security through saving and bounce back from unexpected expenses more quickly. This provides people with more certainty to plan for the future, and enables them to feel confident in the quality of life they will have in older age. Yet, looking at income alone does not give us the full picture. The wider social and economic structures in our society can either reinforce or undermine economic security.

People in Scotland are telling us that the status quo is no longer working. Politicians must show people that these systems, like social security, the labour market and housing, can be redesigned to ensure everyone has the security they need to live a good life.

3. Good work as a foundation for economic security

In Scotland we have seen a steady and significant rise in in-work poverty in the last few decades, with more than 6 in 10 people in poverty having 1 or more person in their household in work (Birt et al., 2025). Working households are not immune to worries about their financial situation. Work can be an important protective factor from economic insecurity for working-age adults. But only if it is good, well-paid and secure.

Focusing on working-age adults, half in work reported that they were feeling economically insecure, rising to 60% for those not in work (and who were not retired). We also find that 4 in 10 (39%) working-age adults not in work were very economically insecure compared to 1 in 4 workers (24%).

We do see slightly more variation in solutions by employment status. People in work have similar priorities, but part-time and self-employed workers are more likely to select more hours (15% vs 8%). Self-employed workers are also more likely to select more predictable pay than employed workers (13% vs 6%). People unable to work due to being disabled are much more likely to select increased social security and more reliable social security (37% and 32% respectively) and less likely to select higher pay. Support with health and wellbeing was consistently selected by around 10-15% of respondents across employment groups, but 1 in 5 people unable to work due to disability selected support for health and wellbeing. Retired people primarily select lower cost of essentials (63%) and improved pensions (49%), 2 of the top solutions across groups.

These findings chime with our previous research on in-work poverty. The labour market is in need of considerable change to ensure that work provides the economic stability that it should. Too many people are in work yet unable to afford the cost of essential things like food and energy. We see that across the income distribution people want to see changes that will enhance their living standards by improving pay and conditions at work and reducing the cost of essentials. Politicians should pay close attention to the public consensus on these solutions, particularly against the backdrop of widespread political disaffection and a looming parliamentary election.

But critically we cannot only rely on work to lift people’s incomes. People who cannot work due to caring responsibility or disability need an adequate and reliable income through social security. The current system is falling short from providing the security it is designed to provide. Government and employers must work together to remove the structural barriers that lock people out of the labour market, support people into good work, and provide a decent income through our social security system for those unable to work.

4. Knowing you will have a roof over your head

We all want a safe and warm home. Yet many people do not feel secure in their home because of financial pressures and insecure tenures. 17% of people said that they were worried about having to move out of their home in the next 12 months because they couldn't afford it. These levels of worry are not unfounded, in the year to September 2025, 33,966 households in Scotland were assessed as homeless or threatened with homelessness (Shelter Scotland, 2026).

We find that feelings of insecurity are more prevalent among private renters (62%) than people with a mortgage or in social rented housing (both 55%). All of these are much higher than the levels of insecurity seen for people who own their homes outright (34%). We also see higher levels of people who are very insecure among renters compared to homeowners.

Housing tenure is a key component of insecurity. Housing costs account for a large share of living expenses, and housing tenure determines these costs and the extent to which people can build economic security through assets. Nearly 1 in 3 (31%) private renters said that they were worried about having to move out of their home in the next 12 months because they couldn't afford it. This is compared to 22% of social renters, 18% of people with a mortgage and 9% of people who own outright.

Social renters tend to have lower incomes than private renters, and are more likely than private renters to be in poverty before housing costs. Housing costs are a bigger driver for private renters, dragging more households into poverty (after housing costs — AHC) because of their housing costs alone. This means it is not surprising that housing costs are a bigger driver for feelings of economic insecurity for private renters than social renters. Additionally, when we consider the greater security of tenure for homeowners and social renters, there exists an additional layer of insecurity for private renters which is likely to intensify feeling of risk if they cannot afford their housing costs.

Younger people are less likely to own and more likely to be private renters. When we look at this pattern by age, for people under 35 we see similar proportions of people feeling economically insecure whether people are renting or paying a mortgage. For people aged 35 and over we see a higher rate of private renters reporting worries about needing to move out of their home because they can’t afford it than for other tenures. More than 1 in 3 (35%) private renting 45-54 year-olds were worried about this compared to 18% of social renters in this age group.

However, when we look at proportions of people who are very insecure by age and tenure we see that younger renters, particularly social renters, are more likely to be very economically insecure compared to older age groups.

This shows that housing costs are a contributing factor across tenures but are a bigger driver of economic insecurity for younger people and for renters across age groups.

Having access to a safe, affordable and good-quality home is a fundamental human right and underpins economic security. Both housing tenure and housing costs directly influence how secure people feel in their day-to-day expenses and their longer-term financial stability. 1 in 10 people reported that housing would be 1 of the top 3 ways to make them feel more economically secure. As you would expect, this varies by tenure, with more than 1 in 4 private renters (27%) prioritising this as a solution that would make them more economically secure.

5. Savings as a safety net

Having a good, regular monthly income can help us feel more secure but it can also help us to build up a safety net for emergencies and for the future. In this section we look at savings, pensions and debt and how they relate to economic security.

Having a lower monthly income makes it more likely to have low or no savings, yet in higher-income quintiles there continue to be households with lower levels of savings. Of people who reported their savings, over half (53%) of people in quintile 1 have savings of less than £250 compared to 13% of people in quintile 5. On the other hand, 1 in 10 people (11%) in income quintile 1 had savings of £50,000 or more. While monthly income can help people to build up savings they do not perfectly overlap. This highlights why it’s important to look across different components of economic security.

Looking at of the proportion of people feeling economically insecure and being very economically insecure we see a clear fall in the proportions feeling economically insecure as they build savings. Around 7 in 10 (68%) people with no savings were feeling economically insecure compared to around 3 in 10 (29%) people with savings of £100,000 or more.

Around £1,000 in savings we see proportions of people being very economically insecure hit the average for the population. Over half (52%) of people with no savings are very economically insecure, compared to 6% of people with saving of £100,000 or more.

The amount of savings that people have also makes a difference to how people feel about other aspects of economic security. Unsurprisingly, we see greater worry about debt for people with less savings, less satisfaction with their savings and less confidence about their future than for people with more savings. For example, 58% of people with no savings are worried about their levels of debt compared to 16% of people with savings of £100,000 or more.

Around half of respondents reported that they had a workplace and/or private pension. Perhaps surprisingly, there is little difference in the proportion of people feeling economically insecure by whether they have a pension or not. We may have expected a wider gap here since pensions are one of the key safety nets in older age. This is likely because other financial buffers, such as monthly income and savings, are what people rely on in the moment, yet pensions provide a safety net for the future, so these are less prevalent in the mind of younger respondents. A second caveat is that in this sample, 1 in 3 respondents without a workplace and/or private pension are aged over 65.

Bearing in mind that this age group generally have lower economic insecurity, this difference may widen further if focusing on working-age adults. The fact that we also see that improved pensions is a top response for both people with and without workplace and/or private pensions also underlines that pensions are more closely tied to economic security than the broader findings suggest.

Underlining that, we do notice clear differences when we look at the proportion that are confident that they will have a decent standard of living in old age. Half (49%) of people with a workplace and/or private pension were confident that they will have a decent standard of living in old age, compared to 40% of people without one.

Shifting our focus from savings to debt, we find that people who are worried about their current levels of debt are more likely to be feeling economically insecure. 8 in 10 (79%) of people who agreed that they were worried about their family’s level of debt are feeling economically insecure, compared to 3 in 10 (29%) of people who disagreed.

Savings are a good indicator of how households are likely to be feeling about their economic security. We see a decline in feelings of economic insecurity and proportions who are very economically insecure as savings increase. In some ways, savings are the result of other components of economic security such as housing, debt and monthly income, and tie these together. Savings also give people the knowledge that they have something to fall back on if they experience an economic shock, either at the individual level (like losing a job) or at the societal level (like the cost of living crisis). Resolving challenges with other components of economic security would enable more families to strengthen their savings and manage unexpected costs and life transitions.

6. Needs and expectations change over the life course

Previous research has shown that feeling economically insecure has a close relationship to the point in a person’s life (Green et al., 2025). This is in part because the components of economic security change over time, but also because people’s feelings about what and how much they need change.

Feelings of economic insecurity peak around the 45-54 age group, with 60% feeling economically insecure and 33% who are very insecure. It is a combination of different components of economic insecurity that is driving this feeling among the 45-54 age group. We see that people in this group are less likely to be satisfied with their savings, less likely to be confident that they will have a decent standard of living in old age, more likely to be worried about building up debt, and more likely to be worried about their income in the next 12 months.

It is in many ways not surprising to see feelings of economic insecurity peak in mid-life as financial responsibilities tend to intensify. We can see that people aged 45-54 are concerned about current financial pressures, particularly as 1 in 3 (32%) reported having savings of less than £250 and are apprehensive about what the future holds.

However, this age group have a relatively even split across the income quintiles, unlike 16-24 year-old who are much more likely to be in the bottom income quintile. This shows that while economic insecurity peaks in mid-life, having a low income is not as much of a driver for that age group as it is for some other age groups.

On the other hand, pensioners have a much lower level of insecurity, this is likely due to higher levels of homeownership as well as higher levels of savings, 46% have savings of £50,000 or more.

When we look at people’s hopes for the future, it’s deeply concerning that only 2 in 5 (44%) adults in Scotland are confident they will have a decent standard of living in their old age. This falls to 1 in 3 (32%) people who are feeling economically insecure and only 18% of people who are very economically insecure.

Adults aged 45-54 years old are the age group who feel least confident about having a decent standard of living in old age, followed by adults aged 55-64 (30% and 40% respectively). While part of this may be due to younger age groups having both thought less about later life and having more time to ‘catch up’, there are clear economic expectations for this age group putting them under financial strains such as mortgage payments and stagnating earnings. We also see that people aged 45 to 54 were less likely to have good levels of savings than other age groups.

There is a clear relationship between household income and feeling confident about your future living standards, with 1 in 3 (34%) in income quintile 1 feeling confident compared to 59% in income quintile 5. Actions taken to improve people's income and wider financial safety net through addressing the building blocks of economic security can ensure a safer and more predictable future. This is not only important for the wellbeing of families in Scotland but is essential for re-building the public’s confidence that politics can create meaningful change.

7. Conclusion

People in Scotland feel like they are skating on thin ice and are losing faith that political decisions will bring about real change. Our analysis across this research series has shown that many people in Scotland are feeling economically insecure and this is driving political disaffection. These 2 sentiments are deeply connected and are not limited by party political boundaries.This is why all political parties should be concerned that many of their voters are feeling disillusioned by politics and the lack of change in their communities.

While the national picture is fragile, we are reaching a critical juncture with the next Scottish parliament election just around the corner. This election, and crucially the next Scottish Government, must focus on tackling poverty and improving economic security for people in Scotland.

We have shown that economic insecurity is shaped by different aspects of people’s lives but is driven by wider social and economic systems. Currently, those systems are not working as they should. The labour market is failing too many people, with many of those who are in work unable to pay for essentials due to a mix of low pay, insufficient hours and insecure contracts. And for those who can’t work, the social security system falls short in providing a sufficient income for a good quality of life.

At the same time, unaffordable and insecure housing, coupled with a persistent cost of living crisis, is fuelling financial precarity for families. Put simply, we must see investment, at scale, to tackle poverty and inequality and improve economic security. Action across these areas would not only ensure people have enough money to cover daily living costs but would also help families build long-term financial stability. There is no time to waste. Politicians must show people in Scotland that a more hopeful and secure future is possible.

Method

This project has been shaped throughout by the End Poverty Scotland Group and includes their words, gathered through qualitative diary entries, throughout. Survey data was collected on behalf of JRF by the Diffley Partnership in November 2025 reaching a representative sample of 3,052 adults (16+) in Scotland.

‘Feeling economically insecure’ is strongly or somewhat agreeing to the statement 'I am worried about me and my family’s economic security' (strongly agree to strongly disagree).

‘Very economically insecure’ is based on people’s mean response across the following questions (strongly agree to strongly disagree):

- I am worried about me and my family’s economic security.

- I am worried about my household’s income over the next 12 months.

- I am worried that I might have to move out of my current home in the next 12 months, because I cannot afford to cover my housing costs.

- I am worried about keeping my job/ I am worried about my ability to get a job (based on employment status).

- I am worried about my current levels of debt.

- I am worried about building up debt in the next 12 months.

- I am generally satisfied with the amount of savings I have (reverse coded).

- I am confident that I will have a decent standard of living in old age (reverse coded).

‘Politically disaffected’ is based on people’s mean response across the following questions (strongly agree to strongly disagree):

- How I vote makes a difference to my life.

- How I vote makes a difference to my community.

- I see positive changes in my community due to political decisions.

- There are politicians who work hard in my area.

- Politicians want to do the right thing, but systems make it hard for them.

- Politicians do not listen to concerns of people like me (reverse coded).

- Politicians care more about their party than the people they represent.

- Even when politicians change, I see no progress (reverse coded).

- Politicians prioritise the concerns of better-off people within society (reverse coded).

- I trust that politicians want to improve the lives of people like me.

References

Birt, C. Cebula, C. Evans, J. Hay, D. and McKenzie, A. (2025) Poverty in Scotland 2025

Green, J. Evans, G. Grant, Z. Inglese, G. and Seibert, L. (2025) Addressing key voters' economic insecurity is vital for all parties

McKenzie, A. and Cebula, C. (2026) Tackling economic insecurity could be key to rebuilding trust in Scottish politics

Shelter Scotland (2026) Homelessness in Scotland

How to cite this briefing

If you are using this document in your own writing, our preferred citation is:

Cebula, C. McKenzie, A. (2026). The building blocks of economic security in Scotland. York: Joseph Rowntree Foundation

This briefing is part of the public attitudes topic.

Find out more about our work in this area.